Contractor vs employee misclassification risks can expose your business to serious legal, financial, and operational consequences—yet many companies still get this fundamental classification wrong. Whether you’re hiring your first contractor, scaling operations across borders, or managing a mixed workforce, understanding how to properly classify workers has never been more critical. Misclassification isn’t just a compliance headache; it can result in back taxes, penalties, lawsuits, and damaged employee morale. This guide walks you through the key differences, global variations, and practical steps to protect your organization.

Quick Summary: Why Contractor vs Employee Misclassification Risks Matter

Before we dive deep, here’s what you need to know right now:

- Classification affects legal liability: Misclassifying contractors as employees (or vice versa) triggers tax, wage, and benefits violations.

- Consequences are costly: Back pay, payroll taxes, penalties, and legal fees can total tens of thousands of dollars per misclassified worker.

- Rules vary by country and region: The US, EU, UK, Australia, and Canada have distinct tests and thresholds; what’s legal in one place may violate another.

- Intent doesn’t matter: Even if you misclassify “by accident,” regulators rarely care—liability still applies.

- Audit risk is real: Tax authorities, labor departments, and worker advocacy groups actively hunt for misclassification schemes.

What Are Contractor vs Employee Misclassification Risks?

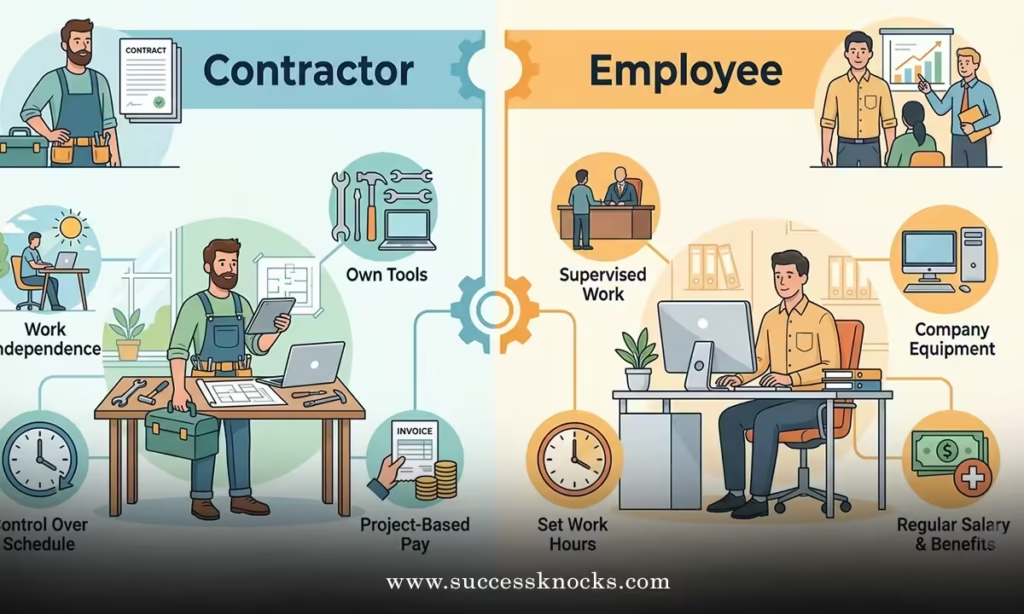

At its core, contractor vs employee misclassification risks describe the legal and financial dangers that arise when a company incorrectly categorizes a worker. The distinction between contractors and employees isn’t arbitrary—it determines whether your business must provide benefits, pay payroll taxes, withhold income tax, and comply with labor laws.

When you hire someone as a contractor, you typically don’t:

- Pay payroll taxes or employer contributions

- Provide health insurance, retirement, or paid leave

- Comply with minimum wage or overtime laws

- Offer workers’ compensation insurance

When you hire someone as an employee, you must do all of the above. The problem? Many business owners blur these lines intentionally (to reduce costs) or unintentionally (from misunderstanding local laws), creating significant exposure.

The Real Cost of Getting It Wrong

Misclassification isn’t a slap on the wrist. If the IRS, Department of Labor, or equivalent agencies in your country discover misclassification:

- Back taxes and interest: You’ll owe payroll taxes for all past periods, plus interest accrual.

- Penalties: Penalties can range from 20–100% of unpaid taxes, depending on intent and jurisdiction.

- Legal fees: Defense costs and settlements from worker lawsuits can exceed $100,000.

- Reputation damage: High-profile misclassification cases attract media attention and erode employee trust.

- Operational disruption: Audits require document production, employee interviews, and management distraction.

Global Contractor vs Employee Misclassification Risks: Key Jurisdictions

Worker classification rules aren’t universal. What’s legal in one country may violate another’s labor code. Here’s how major regions approach this:

United States

The US relies on the ABC Test (adopted by some states) or the common-law Right of Control Test:

- ABC Test (California, New York, others): A worker is an employee unless: (A) the company doesn’t control how work is done, (B) the worker operates outside the company’s normal business, and (C) the worker is independently established in that trade.

- Right of Control Test: If your company controls how, when, and where work happens, the worker is likely an employee—regardless of contract language.

The IRS also uses a 20-factor analysis that weighs behavioral control, financial control, and relationship type.

European Union & UK

Post-Brexit, the UK and EU have slightly different standards, but both lean heavily toward worker protections:

- Worker vs Employee distinction: The EU recognizes a middle category (“worker”) for gig-economy participants who aren’t fully self-employed but still lack employee status.

- Control test: Heavy emphasis on whether the company dictates work methods, hours, and exclusivity.

- Economic reality: Courts ask whether the worker is genuinely in business for themselves or economically dependent on the company.

Recent rulings (e.g., UK Supreme Court on Uber drivers, 2021) have tightened misclassification standards, making it harder to claim contractor status for gig workers.

Australia

Australia uses the Common Law Test, focusing on:

- Control: Does the company control the work method and schedule?

- Integration: Is the work integral to the business?

- Obligation exclusivity: Does the worker have exclusive or near-exclusive ties to the company?

Australian courts have been aggressive in finding employee status, especially in gig economy cases (e.g., Uber BV v Andrianakis, 2017).

Canada

Canada applies a Fourfold Test that considers:

- Control (by the company over the worker)

- Ownership of tools and equipment

- Risk of loss and profit opportunity

- Integration into the business

Canadian courts weight these factors and look for “true independence,” making casual contractor arrangements risky without clear documentation.

Contractor vs Employee Misclassification Risks: Common Scenarios

When Misclassification Happens (And Why)

| Scenario | Why It Happens | Risk Level |

|---|---|---|

| Project-based freelancer who works 40+ hours/week for one client | Appears temporary but shows employee control patterns | High |

| Sales rep paid on commission, no benefits, but required to attend meetings and follow scripts | Company believes “commission = contractor” | High |

| Delivery driver using own vehicle but working exclusive shifts for one company | Assumes vehicle ownership = contractor status | High |

| Virtual assistant working 20 hours/week with flexible schedule | Flexibility misread as independence | Medium |

| Short-term consultant for a specific project, truly independent | Low risk if genuinely independent | Low |

Understanding Contractor vs Employee Misclassification Risks: The Classification Tests

To avoid misclassification, you need to understand which test applies in your jurisdiction and apply it honestly.

The ABC Test (Stricter Standard)

Used in California, New York, and several other US states, the ABC test is presumptively employee-focused. A worker is an independent contractor only if ALL three conditions are met:

A) Control: The hiring company must not control the manner and means of performing the work. B) Scope: The work must fall outside the usual course of the company’s business. C) Independence: The worker must be independently established in an occupation or trade of the same nature as the work performed.

If any condition fails, the worker is an employee.

The Common Law Test (More Flexible)

Used in most US jurisdictions, the UK, Canada, and Australia, this test examines:

- Behavioral control: Does the company direct how the work is done?

- Financial control: Who provides tools, sets rates, and bears the profit/loss risk?

- Relationship type: Is there a written contract, benefits, or ongoing relationship?

No single factor is decisive; courts weigh all factors holistically.

Key Steps to Avoid Contractor vs Employee Misclassification Risks

1. Document the Relationship Clearly

Before bringing anyone on, create a written agreement that specifies:

- Work scope and deliverables (not time commitment)

- Payment terms (fixed fee, per-project, or milestone-based—avoid hourly)

- Schedule flexibility (contractor sets own hours; employee follows company schedule)

- Tool and equipment ownership (contractor provides their own)

- Exclusivity status (contractor can work for others; employee cannot)

- No benefits (contractor waives health insurance, retirement, paid leave)

- Tax responsibility (contractor responsible for self-employment taxes)

- Termination clause (contractor: end-of-project; employee: at-will or per labor code)

A written contract alone won’t save you if practice contradicts it, but it’s essential evidence.

2. Apply the Relevant Test to Your Jurisdiction

- US employees in CA, NY, or other ABC states? All three conditions must be met for contractor status.

- US employees elsewhere? Apply the common law test, weighing all three factors.

- International workers? Research the country where work is performed or where the worker is based.

Don’t assume a contract will override the law. Regulators look at substance over form.

3. Assess Control Realistically

Ask yourself:

- Do I set the worker’s schedule, or do they work when they choose?

- Do I require attendance at meetings, training, or company events?

- Do I provide tools, software licenses, or office space?

- Can the worker refuse assignments without penalty?

- Can they work for competitors?

If you answered “yes” to most of these, you likely have an employee, not a contractor.

4. Evaluate Financial Independence

True contractors:

- Set their own rates (though you can negotiate)

- Invest in tools and training

- Can make a profit or loss on their work

- Work for multiple clients simultaneously

- Invoice for their services

Employees:

- Earn a set wage or salary

- Receive tools and training from the company

- Can’t lose money on their work

- Work exclusively or primarily for one employer

- Receive a regular paycheck

5. Review Regularly and Document

Misclassification isn’t a one-time decision. As relationships evolve, so may classification status. A contractor who initially worked on short projects might gradually transition into exclusive, permanent work—shifting them toward employee status. Review contractor relationships annually and adjust if conditions change.

Contractor vs Employee Misclassification Risks: Common Mistakes & Fixes

Mistake #1: Labeling Someone a Contractor Based on Contract Language Alone

The Problem: A signed contract saying “independent contractor” doesn’t override actual working conditions.

The Fix: Ensure the actual arrangement matches contractor terms. If your “contractor” works 40 hours/week on your premises following your processes, no contract will protect you.

Mistake #2: Confusing “Part-Time” with “Contractor”

The Problem: Many assume part-time or temporary workers are automatically contractors.

The Fix: Part-time doesn’t mean contractor. A part-time employee still receives benefits, payroll taxes, and labor protections. Use the classification test, not the schedule.

Mistake #3: Assuming Tool Ownership Decides Everything

The Problem: “They use their own laptop and phone, so they’re a contractor.”

The Fix: Tool ownership is one factor among many. If you control what they do and when, they’re likely an employee regardless of equipment.

Mistake #4: Ignoring International Variations

The Problem: Hiring a contractor in Mexico or Philippines under US contractor rules.

The Fix: Classify based on the local jurisdiction where work occurs or the worker resides. What’s legal in the US may violate Mexican or Philippine labor law.

Mistake #5: Not Updating as Relationships Change

The Problem: A short-term contractor gradually becomes permanent.

The Fix: Reassess classification annually. If a contractor now works year-round with exclusive focus on your company, reclassify to employee status and begin withholding taxes retroactively if needed.

Action Plan: Avoiding Contractor vs Employee Misclassification Risks

Here’s a step-by-step approach to implement today:

Step 1: Audit Your Current Workforce (Week 1)

List all current contractors and freelancers. For each, note:

- How many hours/week do they work?

- Do they control their schedule?

- Do they work for other clients?

- Do you provide tools, training, or office space?

- Can they be fired without cause, or only if the project ends?

Step 2: Apply the Relevant Test (Week 2)

Research the classification test in your country/state. Apply each factor honestly to each contractor. If you’re unsure, consult an employment attorney.

Step 3: Reclassify if Necessary (Week 3)

If a contractor actually qualifies as an employee, reclassify them immediately. Calculate back taxes, interest, and penalties (or work with an accountant to estimate). You may owe retroactive payroll taxes.

Step 4: Adjust Future Hiring (Ongoing)

For new contractors, use this checklist:

- Written contractor agreement drafted

- Contractor controls their own schedule (no set hours)

- Contractor provides their own tools and equipment

- Contractor invoices for work (not on payroll)

- No company benefits or training provided

- Contractor works for multiple clients

- Contract specifies project-based or termination-for-convenience terms

Step 5: Document Everything (Ongoing)

Keep records of:

- Signed contractor agreements

- Invoices and payment records

- Email communications showing contractor independence

- Project scope and deliverables

- Communications showing the contractor setting their own schedule

Contractor vs Employee Misclassification Risks in Global Teams

If you hire internationally, misclassification risk multiplies. Each country has its own rules, and some are far stricter than the US.

Pro Tips for Global Hiring

- Use local employment law guidance: Consult an employment lawyer in each country where you hire. An hour of advice now saves thousands in penalties later.

- Consider Employer of Record (EOR) services: If hiring abroad, EOR platforms (like Deel, Remote, or Guidepoint) handle local payroll, taxes, and compliance. They take the misclassification risk off your plate.

- Classify conservatively: When in doubt, classify as an employee. The risk of employee misclassification (paying more) is usually lower than contractor misclassification (major penalties).

- Document local laws: Keep a record of the classification test you used and why you chose contractor vs. employee status.

Key Takeaways

- Misclassification happens by accident or design: Even unintentional misclassification triggers serious penalties—intent doesn’t protect you.

- The classification test depends on your jurisdiction: US ABC states, common law states, EU, UK, Australia, and Canada all have different standards. Know which applies to you.

- Control is the biggest red flag: If you control when, how, or where someone works, they’re likely an employee.

- Written contracts aren’t enough: Regulators look at actual practice. A contract saying “independent contractor” won’t save you if the worker operates like an employee.

- Global hiring requires local guidance: Each country has its own rules. Hiring an independent contractor in the US doesn’t make it legal in Germany or Australia.

- Reclassification is expensive but necessary: If you discover misclassification, fix it immediately. Back taxes and penalties are painful, but they’re worse if you ignore the problem and get audited.

- Annual review prevents drift: Contractor relationships that gradually become permanent should be reclassified.

- Professional advice is worth it: Spending $500–$1,500 on an employment attorney’s guidance beats paying $50,000+ in penalties and back taxes.

Conclusion

Contractor vs employee misclassification risks are real, costly, and surprisingly common. Whether you’re building a lean startup, scaling a remote team, or managing global contractors, getting the classification right from day one saves money, legal headaches, and team morale. The good news? Classification isn’t mysterious. By understanding the relevant test in your jurisdiction, assessing control honestly, and documenting the relationship clearly, you can confidently hire contractors without fear of misclassification penalties.

Start this week: audit your current contractors, apply the classification test, and consult an employment attorney if you’re unsure. The small investment in clarity now prevents catastrophic costs down the road. Your team—and your accountant—will thank you.

External References

- IRS Worker Classification Guidance: Official IRS resources on the 20-factor test and classification rules.

- UK Employment Law: Worker vs. Employee Status: UK government guidance on modern employment classification standards.

- International Labour Organization (ILO) – Employment Relationship Recommendation: Global best practices for determining employment relationships.

Looking for the bigger picture? Read our How to Handle Payroll and Tax Compliance for a Global Remote Team

Frequently Asked Questions

Q: Can I hire someone as a contractor to avoid paying payroll taxes?

A: Not legally. If the actual working relationship suggests an employee, the IRS or your country’s tax authority will reclassify them regardless of the contract label. You’ll owe back taxes, interest, and penalties—often exceeding the amount you tried to save.

Q: What’s the difference between a 1099 contractor and an employee?

A: A 1099 is a US tax form contractors file to report self-employment income. Being labeled “1099” doesn’t make someone a contractor; it’s just the tax reporting mechanism. Classification depends on the actual work relationship, not the form used.

Q: If I hire someone overseas as a contractor, do I still face misclassification risks?

A: Yes, absolutely. Contractor vs employee misclassification risks apply in the country where the worker resides and performs work. Hiring someone in the Philippines or Mexico under US contractor rules may violate their labor laws, leaving you exposed to local penalties or claims.

Q: How often should I review contractor classifications?

A: At minimum, annually. If a contractor’s role expands, becomes exclusive, or turns into year-round work, reassess immediately. Gradual relationship drift is how many misclassifications happen.

Q: What’s the safest approach if I’m unsure about classification?

A: When in doubt, classify as an employee. The cost of benefits and payroll taxes (the downside of over-classifying as employee) is usually lower than the penalties from misclassifying someone as a contractor. Alternatively, spend 1–2 hours with an employment attorney to clarify your specific situation.