College costs keep outrunning inflation. In-state tuition at a public university now averages $11,950 a year, out-of-state tuition jumps to $31,880, and private-college tuition hovers near $45,000 before housing and meals. Numbers like these make a tax-advantaged 529 plan essential: money inside grows federal-tax-free and qualified withdrawals stay tax-free. New SECURE 2.0 rules even let savers move up to $35,000 of leftover 529 money into a Roth IRA for the beneficiary.

We analyzed Morningstar’s 2025 medal study (Morningstar), scrutinized every plan’s fee schedule, and combed through dozens of disclosure statements. The result is a ranked countdown of seven direct-sold 529 options that balance low costs, wide investment menus, and meaningful state-tax perks. Here’s how we picked the winners.

How we picked the winners

Choosing a 529 plan shouldn’t feel like tossing darts while blindfolded, so we built a clear yardstick before any rankings began.

First, we relied on Morningstar’s 2025 medal study, the most comprehensive forward-looking review in the industry. Only five direct plans earned a Gold badge that year, and any Gold or Silver rating signaled strong stewardship while screening out weaker programs in one step.

Next, we ran every medalist, plus a few promising Silver contenders, through our own 100-point model. Fees carried the most weight because every basis point you save flows straight to your child’s tuition bill. Bright Start 529’s latest Plan Fee Table shows its index age-based portfolios cost just 0.10 percent per year, while ISS Market Intelligence data on the same page puts the plan’s overall average asset-based fee at 0.24 percent versus a 0.51 percent industry average.

Concrete comparisons like that set the bar for our scoring model and illustrate why low, transparent pricing dominated our rubric. Five-year risk-adjusted returns shared top billing; past performance isn’t everything, yet steady results show the process works. We rounded out the score with investment-menu flexibility, in-state tax perks, user experience, and any extras such as matching grants.

We then double-checked the math. Our team read disclosure statements line by line, confirmed that low advertised expenses weren’t hiding maintenance fees, and verified that each plan stays open nationwide. If a program aced the numbers but stumbled on ease of use, it slipped down the list. A slightly pricier plan with standout customer tools, however, earned a bump upward.

That filter left seven clear front-runners. In the next sections, we’ll count them down, starting with No. 7 and working our way to the plan that gives savers the best shot at outpacing tuition inflation.

7. Alaska 529: active management that earns its keep

Alaska’s plan is the only active-management option in our countdown, and it earns its spot on merit, not sentiment. T. Rowe Price’s multi-asset team guides the age-based portfolios, tilting toward growth stocks when your child is young and moving into bonds as college nears. That tactical approach has outpaced most index-only peers even after fees land around 0.50 percent.

Every underlying fund is a core T. Rowe Price strategy, so you get the same managers and research bench that institutions rely on. Customer service also stands out; hold times are short, representatives understand the glide-path details, and the website is clean and quick, a welcome feature when tuition deadlines approach.

Trade-offs remain. Alaska offers no state tax deduction because the state has no income tax, so residents rely solely on investment quality. Out-of-state families must decide whether potential outperformance justifies the higher expense compared with a low-cost index plan. If you believe skilled managers can add value, or you simply prefer a hands-off, professionally tuned portfolio, Alaska 529 belongs on your shortlist.

6. Virginia Invest529: flexibility meets user-friendly design

Think of Virginia’s Invest529 as a Swiss Army knife for college savings. It offers an option for every saver, from index-only purists to grandparents who want principal protection.

Start with cost. The passive age-based portfolios hold expenses near 0.18 percent, keeping more growth compounding in your child’s name. Prefer active management? Switch to American Funds tracks or build a custom mix without leaving the platform. If college is close and you feel uneasy about market swings, park cash in the Stable Value Portfolio, which currently yields more than many high-street savings accounts.

Virginia layers on resident perks. Parents can deduct up to $4,000 per account each year, and contributors age seventy or older face no deduction cap. Another twist: the Tuition Track Portfolio lets Virginians lock in credits that rise with in-state tuition, giving you prepaid certainty inside a modern 529 wrapper.

The interface keeps tasks simple. The dashboard separates each beneficiary, tracks tax-deduction limits in real time, and allows one-click withdrawals when bursar bills arrive. Reliable phone support and a polished mobile app round out a plan built to serve families from diaper days through diploma day.

5. Pennsylvania 529 Investment Plan: Vanguard index power with tax parity

Pennsylvania’s direct plan stays simple: Vanguard index funds under the hood, low expenses, and performance that often lands in Morningstar’s top quartile. Costs for its age-based tracks sit near 0.20 percent, leaving more of your money compounding for tuition.

The real differentiator is a generous, flexible tax break. Residents can deduct up to $19,000 per beneficiary each year (double for married filers). The deduction applies to contributions in any state’s 529, yet the home plan already checks every major box, so Pennsylvanians rarely look elsewhere.

Investor safeguards add comfort. State law protects 529 balances from creditors, and there is no minimum to open an account. The web portal mirrors Vanguard’s clean layout, making contributions, reallocations, and gifting easy—even for less tech-savvy grandparents.

Trade-offs exist. The lineup is strictly index-only, so fans of active funds will need another state. Out-of-state savers who want the absolute lowest fee can shave a few basis points by choosing New York. If you value Vanguard stewardship paired with standout state incentives, Pennsylvania 529 is a strong contender.

4. New York 529 College Savings Program: rock-bottom fees, zero fuss

If you want low costs to do the heavy lifting, New York’s plan is hard to beat. Every portfolio—age-based or static—uses Vanguard index funds, and the state’s asset scale holds total expenses near 0.12 percent. That equals about $1.20 per year for every $1,000 invested, so more of your money keeps compounding for tuition.

Simplicity is the other draw. The menu offers three risk tracks that glide from stocks to bonds as college nears. No niche options and no complex decisions, which suits parents who prefer a true set-it-and-forget-it approach.

Residents gain an additional perk: up to $10,000 in state-tax deductions each year on contributions. Out-of-state families do not receive that break, yet many still choose New York for the fee advantage and the plan’s easy online gifting tools.

The trade-off is variety. You will not find active funds, ESG themes, or custom-mix sliders. It is index-only, take it or leave it. For most savers, that focus on cost efficiency is a benefit, and it secures New York’s place in our top four.

3. Massachusetts U.Fund: Fidelity’s low-cost index factory

The U.Fund attracts savers for one reason: it makes college investing feel effortless. Fidelity runs the program, and every age-based track uses broad-market index funds that cost about 0.12 percent per year. That tiny drag leaves more tuition money compounding quarter after quarter.

Opening an account is simple. If you already hold a 401(k) or brokerage at Fidelity, the 529 appears next to those balances. One login, one mobile app, and a set-and-forget automatic draft create a seamless routine.

Investment choice stays streamlined by design. Select an aggressive, moderate, or conservative glide path and the portfolio adjusts on schedule. Prefer a static mix? Six fixed-allocation options range from all-equity to mostly bonds, plus a principal-protected track for nervous savers approaching freshman year.

Massachusetts adds up to $2,000 in state-tax deductions per household each year. While not the richest perk on our list, pairing that break with rock-bottom fees and Fidelity’s customer support places U.Fund firmly in our top three.

2. Utah my529: customizable power with Vanguard-level pricing

Utah’s my529 has carried a Morningstar Gold badge for more than a decade, and the strengths appear the moment you log in.

Costs first. A standard age-based index track runs about 0.12 percent. That is only slightly higher than New York’s bargain fee yet gives you far more control. Hands-off investors can pick from four prebuilt glide paths, while power users can build a custom mix from Vanguard and Dimensional funds in one-percent increments. Want 70 percent U.S. stocks, 20 percent international, and 10 percent TIPS? Click, save, finished.

Flexibility extends to contributions. After the initial $25 deposit, there is no minimum. The plan works with payroll direct deposit, Ugift codes for birthdays, and a mobile dashboard that tracks progress toward college and alerts you when 529-to-Roth rollover rules might unlock extra benefits.

Utah residents receive a 4.45 percent state-tax credit on contributions (up to about $5,120 per child each year for joint filers). While not the largest perk on our list, pairing that credit with low fees and top-quartile returns makes my529 the default choice for locals and a compelling out-of-state option for investors who want customization without advisor-sold markups.

1. Illinois Bright Start: gold-medal champion with ultra-low fees

Illinois moved from middle of the pack to first place after a broad overhaul cut costs and widened investment choice. An all-index age-based portfolio costs about 0.10 percent. On a $50,000 balance, that equals roughly $50 a year for full portfolio management.

Bright Start also breaks the single-fund-family mold, and its education center offers a straightforward college savings options comparison that underscores perks like Illinois’s tax deduction and tax-free withdrawals over Roth IRAs or a basic savings account. Vanguard, DFA, T. Rowe Price, and BlackRock sit side by side, so you can blend styles without opening multiple accounts. Prefer a plain index glide path? Select it and move on. Want a splash of small-cap value or international real estate? Pick from the menu without extra paperwork.

Illinois residents enjoy one of the most generous flat deductions in the country: up to $20,000 in contributions per couple each year. At the state’s 4.95 percent income-tax rate, that is nearly $1,000 back, enough to offset a hearty stack of textbooks.

The website adds helpful touches. Color-coded goal meters show how much tuition you have already “purchased,” and quarterly rebalancing keeps risk in line.

Combine ultra-low fees, multi-manager choice, and a strong tax break, and Bright Start secures the top spot in our 2026 rankings.

Honorable mentions and niche gems worth a look

Seven plans made the main list, but a few others excel in special situations. Treat them as small-batch options with unique advantages.

Louisiana’s START Saving Program stands out for residents. The state adds an earnings-enhancement match of up to 14 percent on yearly contributions, combines that with zero program fees, and invests in Vanguard index funds. For families whose ZIP code begins with 7-0, START can deliver exceptional value.

Arkansas’s Brighter Future 529 often flies under the radar. Fees sit slightly above national leaders, yet the state encourages employers to help you save by granting them a $500 business-tax deduction when they match your contributions. An employer match frequently outweighs shaving a few basis points from expenses.

Alaska’s University of Alaska Portfolio offers a hybrid prepaid-savings twist. Contributions are guaranteed to track in-state tuition, so a student intent on studying under the northern lights can lock in today’s prices and sidestep future inflation.

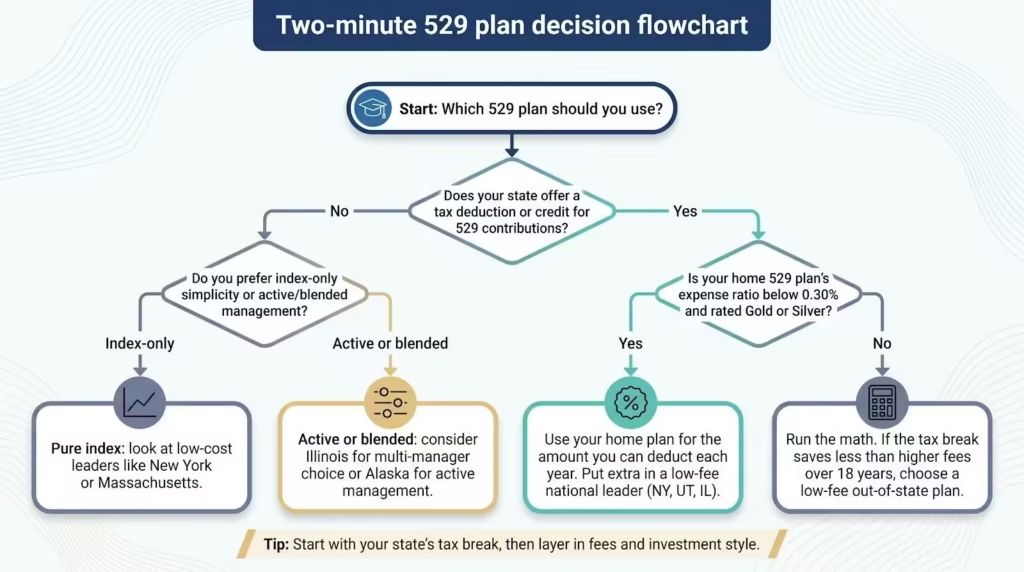

A two-minute flowchart: should you stay in-state or go national

- Does your state offer a tax deduction or credit for 529 contributions?

- Yes → Go to step 2.

- No → Skip to step 3.

- Is your home plan’s total expense ratio below 0.30 percent and rated Gold or Silver?

- Yes → Use the home plan for the amount you can deduct each year. Invest any extra in a low-fee national leader (NY, UT, IL).

- No → Run the math. If the deduction saves less than the fee gap over 18 years, choose an out-of-state plan.

- Do you prefer index-only simplicity or active management?

- Pure index → New York or Massachusetts keeps costs low.

- Active or blended → Consider Illinois for multi-manager choice or Alaska if you believe T. Rowe Price can outperform.

Follow these forks and you will land on a shortlist that fits both your ZIP code and your investing style, with no actuarial tables required.

Conclusion

Begin with your own state’s tax benefits and plan rating. If you live in a no-income-tax state or qualify for a rare perk like Louisiana’s match, these niche programs may stretch your college dollars further.